")

Introduction

Table of Contents

Manufacturing transforms raw material into finished commodities. During transformation, the process pits two cost categories, i.e., prime costs vs. conversion costs. Prime costs are expenditures directly attributable to finished products. Conversion costs comprise all expenses of turning raw materials into the desired product.

What are Prime Costs?

Prime costs comprise expenditures incurred directly in creating a finished product or service. Direct labor, direct material, and direct expenses are the three elements of prime costs. Factory overheads and administrative costs are not included in this category. Prime costs are also direct costs.

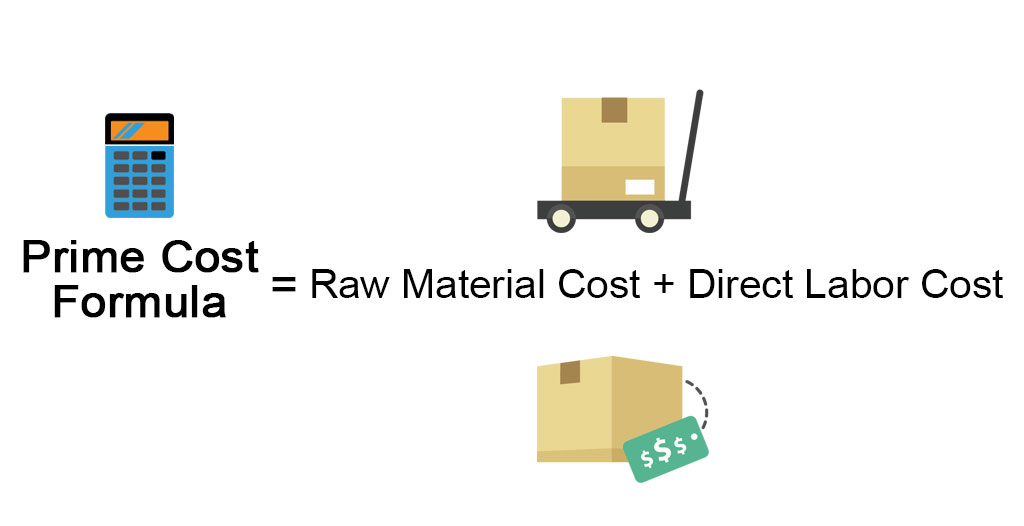

1- Prime Cost Formula – How to Calculate it

To calculate the prime cost, sum up all direct costs as shown below:

Prime Cost = Direct Material Costs + Direct Labor Costs + Direct Expenses

The following formula also applies:

Prime Cost = Direct Labor + Raw Material Cost

The balance sheet of a manufacturing entity has these costs. To compute,

- Locate the entry showing direct raw materials cost.

- Do the same for direct labor costs.

- Add the two figures to arrive at the prime cost.

2- Prime Cost Examples

- Direct materials include every aspect of material put in a finished product. Examples include rubber used in tire manufacture, lumber, paint, and hardware used to make furniture.

- Salaries and wages paid to personnel associated with the product or service

- Indirect costs such as delivery, utilities, and salaries paid to managers are excluded due to the difficulty of quantifying and allocating to the finished product.

3- Use of Prime Cost

Prime cost analysis provides a manufacturing entity with a cost reduction model for maximum profit realization. It also helps in maintaining efficiency during production. A prime cost is also the direct cost of a product. Manufacturers can lower their prime costs to either increase profit or undercut the competition. For small-scale producers, prime cost computation assists them in monitoring hourly wages earned and profit per unit produced.

4- Advantages of Prime Cost

- Prime cost quantifies direct labor, direct material, and all direct expenses incurred in a product’s manufacture.

- Prime cost avoids overhead expenses, which are sometimes difficult to attach to a product.

- Prime cost analysis assists manufacturers set product prices that result in a desirable profit.

What are Conversion Costs?

Conversion costs are the expenditures incurred in transforming raw materials into finished or partially complete products. They comprise metrics like administrative expenses, factory overheads, and direct labor costs incurred in the conversion process.

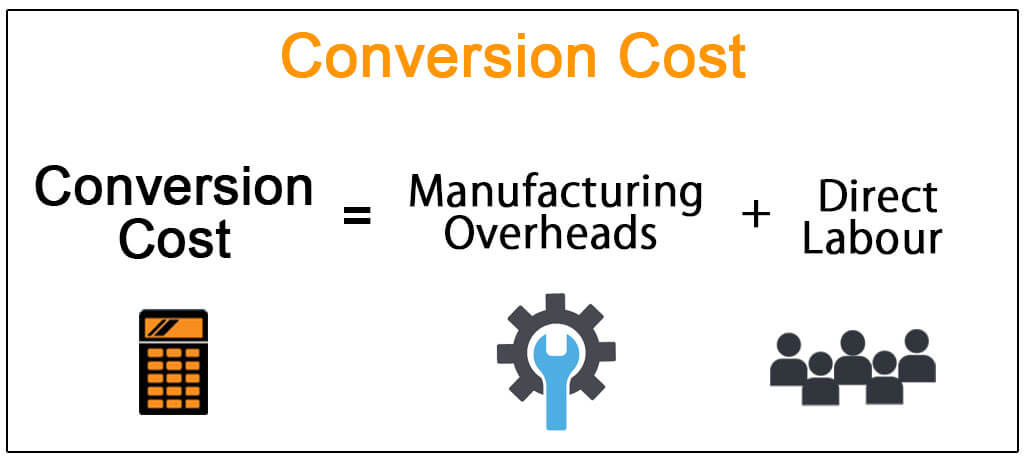

1- Conversion Costs Formula – How to Calculate it

To compute conversion costs, take direct labor cost and add the overhead cost as shown below:

Conversion Cost = Direct Labor + Overhead cost

Overhead costs are incurred to keep operations running and include elements like electricity, telephone, and postage. Direct labor comprises costs like salaries, staff insurance, and pension.

2- Conversion Costs Examples

Direct labor is the monetary value of input from workers involved in turning raw materials into a product. Examples include salaries and wages paid to factory staff, bonuses, pension fund contributions, insurance, etc.

Manufacturing overheads under conversion costs are portions attributable to the unit production process. Examples include electricity, insurance, machine repair and maintenance, depreciation, and taxes.

3- Use of Conversion Costs

Conversion costs, as noted earlier, bring together all expenses that go towards adding value to raw material. Awareness of these costs provides an insight into what a manufacturing entity spends on inventory production.

Conversion costs assist in estimating production expenses while also estimating utilized inventory and what is in stock. Conversion costs gauge a company’s production efficiency, which helps minimize wastages.

Conversion costs allocate overheads that prime costs avoid. Allocation of overhead costs ensures proper monitoring and cost planning.

Conversion cost calculations act as a determinant for the cost of sales figure that goes to the income statement.

4- Advantages of Conversion Costs

- Conversion costs determine the actual expenditure committed towards a finished product. Managers can accurately measure what a finished product incurs.

- Conversion costs help eradicate production deficiency. By computing these costs, managers develop a monitoring model to guide them in reducing production costs in the future.

- Conversion costs help in modeling the cost of goods manufactured, resulting in a realistic price setting.

FAQ: Is Direct Labor Considered Both a Prime and a Conversion Cost?

Direct labor goes both ways. When computing prime costs (Prime cost = Raw Material Cost + Direct Labor Cost), direct labor is one of the elements. Likewise, conversion cost computation (Conversion Cost = Direct Labor + Overhead Cost) requires direct labor as an input.